How to Use Bond Ladders for Stable Retirement Income in 2025

Using bond ladders can be an effective strategy for generating stable retirement income in 2025. By purchasing bonds with varying maturities, retirees can ensure a consistent cash flow while minimizing interest rate risk. This approach allows for reinvestment opportunities and helps maintain liquidity, making it easier to adapt to changing financial needs throughout retirement.

As you approach retirement, ensuring a steady stream of income becomes paramount. One strategy that can help achieve this goal is utilizing a bond ladder. A bond ladder is a fixed-income investment strategy that involves purchasing bonds with varying maturities to create a consistent income stream over time. Here’s how to effectively implement a bond ladder for stable retirement income in 2025.

What is a Bond Ladder?

A bond ladder consists of multiple bonds that mature at different intervals, typically ranging from 1 to 10 years. This method allows investors to take advantage of interest rate changes while providing liquidity as bonds mature. As each bond matures, the principal can be reinvested into a new bond, maintaining the structure of the ladder. This strategy is particularly beneficial for retirees looking for stable cash flow without being overly exposed to interest rate fluctuations.

Benefits of Using a Bond Ladder

Implementing a bond ladder has several advantages, especially for retirees:

- Consistent Income: A bond ladder provides a predictable income stream as bonds mature at regular intervals.

- Interest Rate Risk Mitigation: By holding bonds with different maturities, you can reduce the impact of interest rate fluctuations on your overall portfolio.

- Reinvestment Opportunities: When bonds mature, you have the option to reinvest in new bonds, potentially at higher rates.

- Liquidity: Regular maturities give you access to cash, which can be critical for covering unexpected expenses.

Building Your Bond Ladder

To create an effective bond ladder, follow these steps:

1. Determine Your Income Needs

Assess your expected expenses in retirement to understand how much income you need from your bond ladder. A common rule of thumb is to aim for a bond income that covers at least 70-80% of your annual expenses. This will help you determine the total investment required in bonds.

2. Choose Your Bond Maturities

Decide on the number of rungs in your ladder and the maturity lengths. A typical ladder might consist of bonds maturing in 1, 3, 5, 7, and 10 years. This diversification helps balance short-term liquidity with long-term growth potential.

3. Select Bond Types

Consider various types of bonds for your ladder, such as:

- U.S. Treasury Bonds: Low-risk bonds backed by the government.

- Municipal Bonds: Tax-advantaged bonds issued by local governments.

- Corporate Bonds: Higher yield bonds from private companies, though they carry more risk.

4. Purchase Bonds

Once you’ve selected the bonds, purchase them through a broker or directly from the issuer, ensuring they fit your investment strategy. Make sure to also consider the credit ratings and the financial health of the bond issuers.

5. Monitor and Adjust

Regularly review your bond ladder to ensure it continues to meet your income needs and risk tolerance. Be prepared to make adjustments as market conditions change, such as reinvesting matured bonds or selling underperforming bonds.

Chart: Example of a Bond Ladder

Below is a simplified example of a bond ladder illustrating different maturities and their respective yields. This example assumes an investment of $100,000 spread evenly across five bonds:

| Maturity | Bond Type | Investment Amount | Annual Yield (%) | Annual Income |

|---|---|---|---|---|

| 1 Year | U.S. Treasury | $20,000 | 2.0 | $400 |

| 3 Years | Municipal | $20,000 | 2.5 | $500 |

| 5 Years | Corporate | $20,000 | 3.0 | $600 |

| 7 Years | Municipal | $20,000 | 3.5 | $700 |

| 10 Years | U.S. Treasury | $20,000 | 4.0 | $800 |

The total annual income from this bond ladder would thus be $3,000, providing a stable income stream throughout retirement.

Conclusion

Using a bond ladder can be a valuable strategy for retirees seeking to secure stable income in 2025. By understanding how to build and manage your ladder effectively, you can enjoy peace of mind knowing that your financial needs will be met throughout your retirement years. As always, consider consulting with a financial advisor to tailor your bond ladder to your specific situation and goals.

Explore

Mastering Your Income Tax: The Ultimate Guide to Online Advice

Best Passive Income Ideas to Grow Your Wealth in 2025

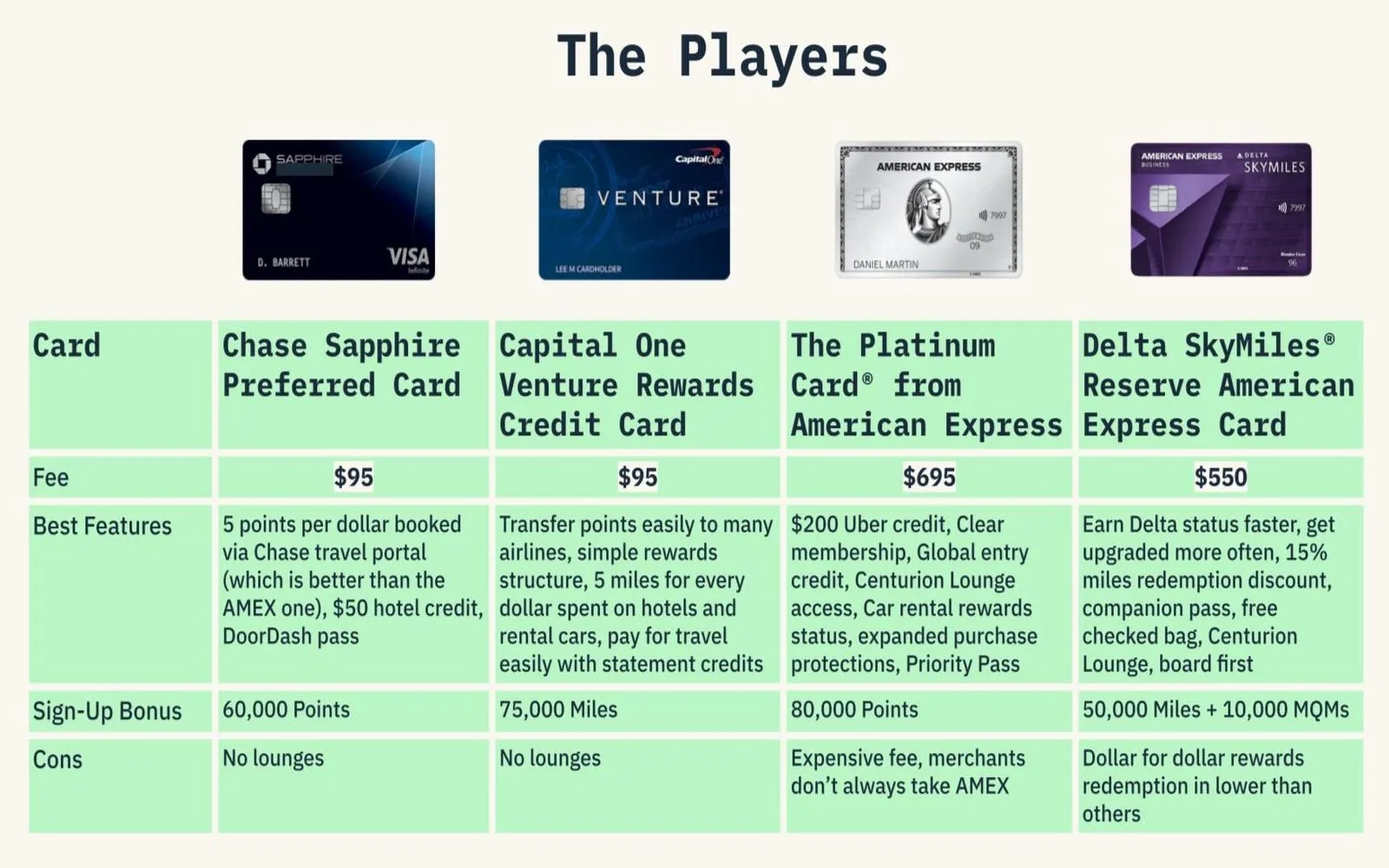

Maximize Your Savings: How to Use Credit Card Points for Affordable Flights in 2025

Top Small Business Management Tools to Use in 2025

Top Roth IRA Options for 2025: Secure Your Retirement with the Best Plans

Top 401(k) Providers with Low Fees for 2025: Maximize Your Retirement Savings

Guide to Finding the Best Retirement Advisor for 2025

Best Crossovers SUVs of 2025